Can Doctors & Dentists Get 100% Financing? A Guide to Healthcare Practice Loans

Last updated April 2026

One of the biggest advantages healthcare professionals have is access to financing that looks very different from traditional small business lending.

Banks often view physicians, dentists, and other licensed providers as a distinct category of borrower. Because of their earning potential, demand stability, and repayment track record, many lenders have built specialized programs, some of which include up to 100% financing for practice acquisitions, buy-ins, startups, and even personal home purchases.

But “100% financing” doesn’t mean what most people think and it’s not always the right move.

In our experience, most first-time buyers focus too much on whether they can get 100% financing and not enough on whether they should.

Quick Answer: Can Healthcare Providers Get 100% Financing?

Yes many lenders (such as Huntington Bank) will offer up to 100% financing for qualified healthcare professionals, especially for:

Buying an existing practice

Buying into a group

Certain equipment or buildout costs

However, approval comes down to:

Your credentials and experience

The strength of the practice

Your overall financial position

👉 Simple version:

The more proven and visible the deal is, the more comfortable a bank becomes financing it fully.

What 100% Financing Actually Means (In Plain English)

When lenders say 100% financing, they are typically saying:

“We’re willing to fund the full project cost without requiring a traditional down payment if the deal holds up.”

What it can include:

Practice purchase

Buy-in ownership

Equipment

Tenant improvements

Sometimes working capital

What it does NOT mean:

No underwriting

No credit requirements

No need for cash reserves

No risk to you

What this means for you:

You may not need to bring $100K–$300K+ upfront

You can preserve cash for:

Living expenses

Ramp-up period

Unexpected costs

👉 Key takeaway:

100% financing is not “easy money” it’s confidence-based lending tied to your profile and the deal itself.

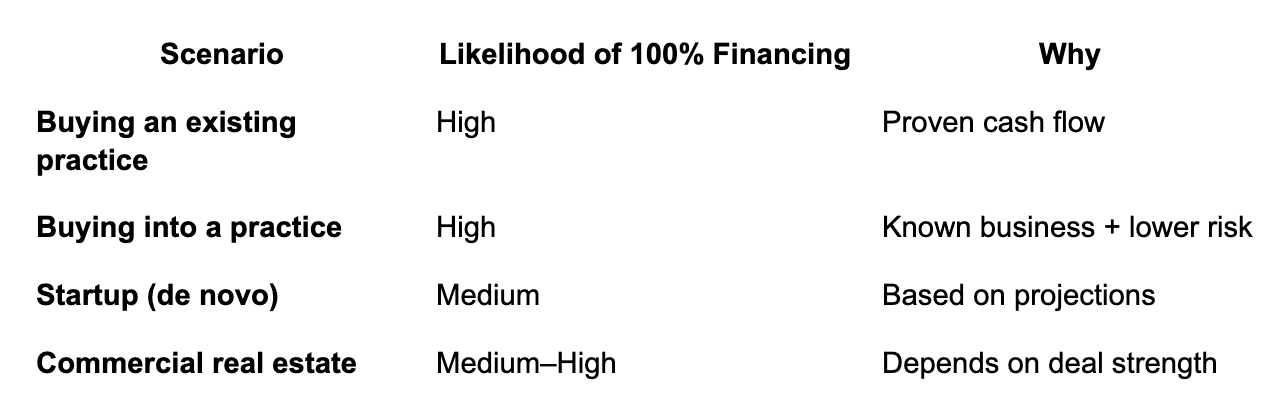

When You’re Most Likely to Qualify for 100% Financing

Not all deals are viewed equally.

👉 What this means for you:

If leverage is important, buying or buying in is usually far easier to finance than starting from scratch.

Why Buy-Ins and Acquisitions Are Easier to Finance

This is where lenders think very differently than most providers expect.

Startup practice

The bank is evaluating:

Will patients come?

Will revenue ramp fast enough?

Will everything execute correctly?

👉 Translation: more unknowns = more risk

Buy-in or acquisition

The bank can see:

Real patient volume

Historical collections

Staff already operating

Proven location

👉 Translation: less guessing = more confidence

What this means for you:

When you buy or buy in:

You’re stepping into an existing system that works

You’re reducing uncertainty for the lender

That’s why banks are more willing to:

Offer higher leverage (including 100%)

Provide better terms

Move faster

A Real-World Example

Dentist A: Startup

New office

No patients yet

Full buildout + marketing

👉 Bank view:

“We’re betting on projections”

Dentist B: Acquisition

$800K purchase

~$200K earnings

Established patient base

👉 Bank view:

“We can see exactly how this performs”

Result:

Dentist B is far more likely to:

Get 100% financing

Receive stronger terms

Close faster

👉 The rule is simple:

The more a bank can see, the more it’s willing to lend.

What Lenders Actually Care About (Even With 100% Financing)

Even in specialized programs, lenders still look at fundamentals.

Typical benchmarks:

DSCR: ~1.20x–1.30x+

Global cash flow: total income vs obligations

Liquidity after closing

They’re evaluating:

You

Credentials

Experience

Credit

The business

Cash flow or projections

Patient mix

Location

The deal

Structure

Working capital

Sustainability

👉 Important:

100% financing doesn’t remove risk, it shifts how the bank evaluates it.

How This Impacts Your Personal Financial Life

This is where people get surprised.

At the same time you’re:

Buying a practice

Taking on business debt

You may also want to:

Buy a home

Yes, you can often do both

Healthcare-specific loan programs may allow:

Low or no down payment

No PMI in some cases

Flexibility with student loans

But here’s the reality:

We’ve seen situations where someone gets approved for both a practice and a home and feels financially tight within 6–12 months because no one walked through the full picture.

What you should actually think about:

Monthly obligations after closing

Cash left in the bank

Time to stabilize the practice

Lifestyle costs

👉 Approval is not the hard part. Living with the decision is.

Where People Get This Wrong

This is where mistakes tend to happen:

Chasing 100% financing because it sounds good

Not thinking about life after closing

Assuming all lenders evaluate risk the same way

Underestimating how long a startup takes to stabilize

👉 The biggest mistake:

Optimizing for approval instead of optimizing for sustainability.

How to Approach Financing the Right Way

The strongest borrowers think beyond just getting approved.

1. Talk to multiple lenders

Not all banks think the same, especially in healthcare.

2. Understand your full financial picture

Not just the loan, your entire balance sheet.

3. Don’t chase max leverage blindly

Sometimes less leverage = better flexibility.

4. Align financing with your stage

Startup → more conservative

Buy-in/acquisition → more aggressive options

5. Protect your liquidity

Especially in the first 12–24 months.

Frequently Asked Questions About Healthcare Practice Financing

Can dentists get 100% financing to buy a practice?

Yes many lenders will offer up to 100% financing for qualified borrowers purchasing established practices with strong cash flow.

Is it easier to finance a buy-in or startup?

Yes. Buy-ins and acquisitions are typically easier because they have proven revenue.

Can I buy a practice and a home at the same time?

Yes but managing total debt and liquidity is critical.

Do I need any money at all?

Not always but having reserves is still important for stability.

Final Thoughts

Healthcare financing is different because healthcare risk is different.

That’s why:

Banks offer specialized programs

Some allow up to 100% financing

Approval can look very different than traditional lending

But the real question is not:

“How much can I borrow?”

It’s:

“What structure sets me up to succeed long-term?”

Because on paper, a deal can look perfect.

In real life, it has to feel manageable every month.